An Nvidia Blowout Quarter is More Important Than Ever

Nvidia (NVDA) sits at the crossroads between artificial intelligence (AI), big data, cryptocurrencies, and anything and everything in need of high-powered chips.

On one hand, this translates into the company putting out more press releases and blog posts than nearly any stock covered by analysts like myself. On the other, this unique position delivers gains time and time again for shareholders.

Year-to-date, shares of the graphics card maker are up 159%!

Not to mention, over the past month, shares of Nvidia have rumbled more than 41% higher from their August 5 lows of $90.69.

But one of the world’s biggest wealth creators in recent years faces its next hurdle this evening when it reports second quarter earnings.

Let’s be honest…

Nvidia’s business is humming along. In the first quarter, total revenue rose 262% to a record $26 billion. Meanwhile, earnings jumped 461% to $6.12 per share.

Data center revenue was the big driver, surging 427% to $22.6 billion. This offset some stalling growth from its former crown jewel, its Gaming and AI PC segment, which only saw an 18% year-over-year increase in sales.

But with the unveiling of Blackwell and a number of expanded partnerships with AWS, Google Cloud, Microsoft (MSFT) and Oracle (ORCL), there was plenty to be excited about from the results.

As the company’s leather jacket-wearing founder and CEO, Jensen Huang stated, “The next industrial revolution has begun — companies and countries are partnering with NVIDIA to shift the trillion-dollar traditional data centers to accelerated computing and build a new type of data center — AI factories — to produce a new commodity: artificial intelligence. AI will bring significant productivity gains to nearly every industry and help companies be more cost- and energy-efficient, while expanding revenue opportunities.”

Nvidia also announced a 150% increase in its dividend per share, as well as a 10-for-1 stock split… which we here knew was coming.

Shares of Nvidia jumped 9.8% on first quarter earnings, in line with the +/- 9% move I said the options market anticipated and better than the 5.82% move VertEA forecast.

With that background, what’s in store for this evening…

A Tepid Response?

Let’s start with the good news…

Historically, Nvidia shares perform well in August.

From 2005 to 2023, they’ve only ended the month with a loss four times. That’s a 78.9% chance for success. And they’re currently up more than 7.5% in 2024.

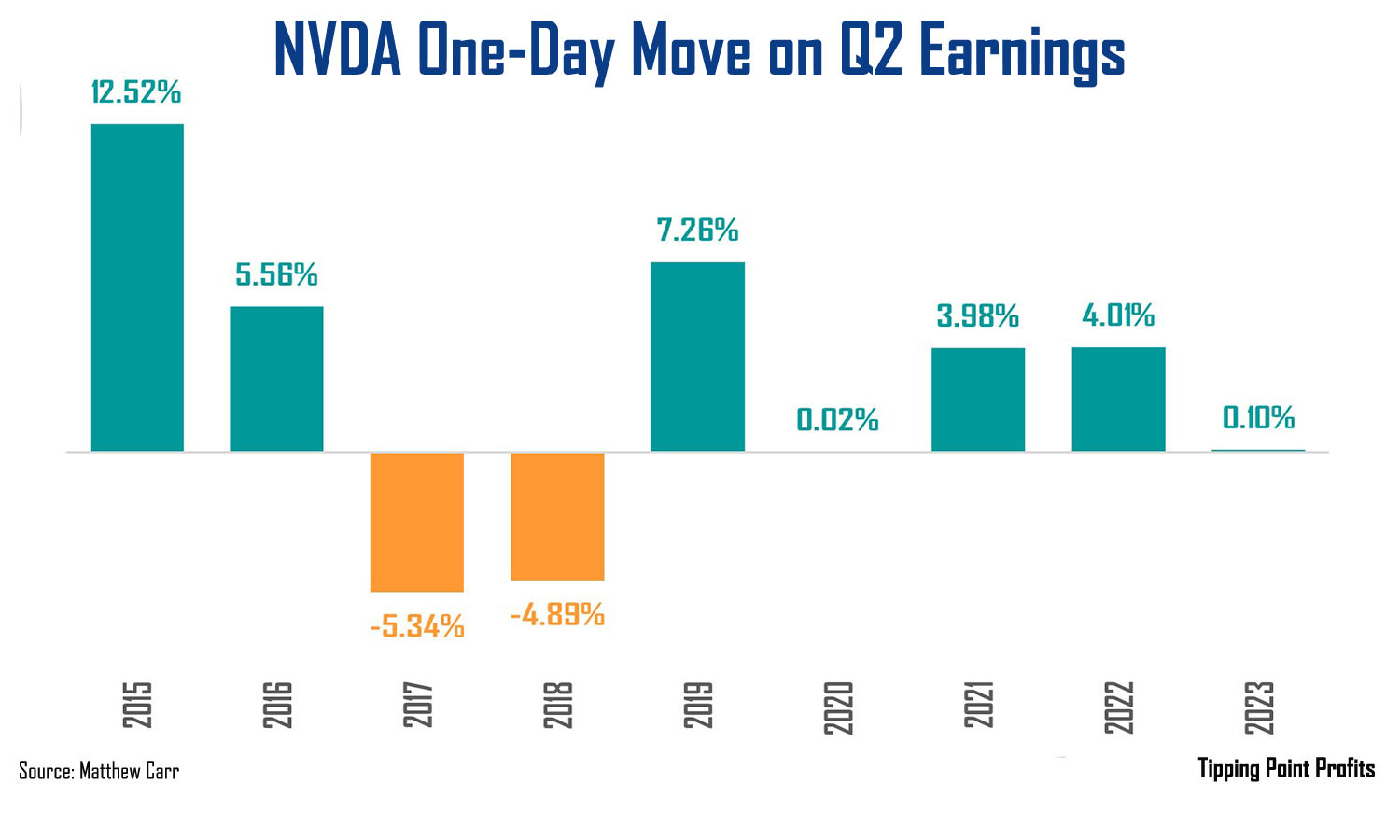

Now, when using VertEA we see that Nvidia shares have only fallen on second quarter results twice since 2015…

They’ve risen five consecutive years on this report. Though two – 2020 and 2023 – were marginal.

But our average one-day move on second quarter earnings since 2015 is a gain of 2.58%. That makes it the worst received report during that span.

The current projected move from the options market is +/- 9.9%. That means a jump to $141 or a drop to $115.85.

Much like I said during first quarter results, it’s also worth noting that over the past five earnings releases from Nvidia (going back to first quarter 2023) our average one-day move on is 9.55%.

That’s the positive.

But here’s where things get a little tricky…

For the second quarter, Wall Street is expecting Nvidia’s revenue to rise 112% from $13.51 billion to $28.68 billion. This would be a new record. And earnings per share are forecast to increase 140% to $0.65.

The company’s data center segment is projected to see a 142% increase in revenue to $24 billion with its gaming segment chipping in $2.7 billion.

So, everyone on Wall Street is expecting Nvidia to top these numbers, as well as raise third quarter guidance. That’s even with the Blackwell delays and design flaws the company is working to get back on track. The consensus is it’s Hopper bookings have offset this short-term shortfall.

But we do see that the growth for Nvidia – which is still tremendous – is entering a period where the comparables become more difficult. I mean, a forecasted 142% increase in data center business is fantastic. And hyperscalers are projected to dump $500 billion over the next two years building out the infrastructure.

The downside is that’s a cooling off from the 427% growth for Nvidia’s data center segment seen in the first quarter. This could cap any upside move.

Now, Nvidia hasn’t had a real misstep on earnings since the fourth quarter of 2021. Shares have dipped on third quarter earnings the past two years. But nothing major. For instance, in third quarter of 2023 the fundamentals were fine, but the company warned export restrictions were impacting sales to China and gave a cautious tone for the fourth quarter. Shares ended the day down 2.46%.

There are times when the hopes and dreams of investors are pinned on a single company.

And as long as that company performs well, all is right in the world… well, as much as the world that can be.

No corporate entity embodies this more at the moment than Nvidia.

The sheer cacophony of voices talking about the chip maker… the library of analysis that’s been written in anticipation of this earnings report (mine included) is a testament to this.

All of Wall Street is expecting a beat and raise. It better be… Or there will be hell to pay.

Still bullish on Nvidia,

Matthew

Glad to hear that you are still bullish. I agree!

Of course!