Is It Time to Flee This Falling Knife or Get Out the Catcher’s Mitt?

If you’ve ever worked in a kitchen, you’ve undoubtedly heard the phrase, “A falling knife has no handle.”

We’re taught that when a knife drops to instantly raise our hands above our heads.

The reason is purely psychological.

It’s to counter our innate instinct to try and catch something that’s falling or that we’ve dropped… whether it's an apple, a koosh ball, a chainsaw, or a knife sharpened to the finest of edges.

So, we’re trained to raise our hands in mock surrender to prevent unintentionally hurting ourselves.

In investing, that same advice is given to avoid financial maiming… “Don’t try to catch a falling knife.”

A plummeting stock can be just as deadly as a real-world tumbling blade.

But is there a way to tell the difference between something dangerous and a discounted opportunity?

Because at some point, all falling knives must be safe to pick up again… right?

Eagle Pose Empire

Yoga pants.

Back in the late 1990s, few would’ve pegged that as a multi-billion-dollar idea.

But one forward-thinking company sure did.

And Lululemon (LULU) has gone on to become one of the greatest corporate success stories of the past 25 years. The Canadian athletic apparel brand has seen its revenue grow from $350 million in 2008 to $9.6 billion in 2023.

That’s a staggering 2,642% increase!

And since 2020, Lululemon’s annual revenue has more than doubled.

Plus, the company has a plan in place to double 2021’s revenue by 2026… That would mean an increase to $12.5 billion.

Already, its iconic yoga pants paint bottoms from North America to Europe to Asia and Oceania… well, at least that’s what the company wants you to believe.

Let’ 's be honest though… more than 66% of Lululemon’s global sales come from the U.S. If we add its home country Canada to that total, we get 80% of all the company’s revenue.

So, yes, it’s technically a global athleisure company… but with an asterisk.

Now, with the success Lululemon has had increasing revenue over the past several years, some investors may start scratching their heads when they pull up a price chart for shares.

The two don’t mesh.

You see, shares of Lululemon set a new 52-week high of $516.39 back in December.

But since then, they’ve shed more than 40% of their value.

And in May, they set a new 52-week low of $293.03.

That’s a troubling about-face over six months for shareholders.

And the surface, this feels like that “falling knife” the kitchen manager and Wall Street wisdom are always warning us about.

But let me say, that a lot of this decline is typical for what we see from Lululemon shares.

For instance, the company reports third quarter earnings in December… and shares have fallen on this report five out of the last six years.

Next, Lululemon shares have tumbled in January for four consecutive years. They’ve ended February and March down three of the past five.

And May is notorious for being the worst month of the year for the athletics apparel company. Shares have ended the month lower 12 of the past 17 years, including 8 of the past 10, and the last four years consecutively. Not to mention, for the last three years, shares of Lululemon have fallen at least – AT LEAST - 12.8% in May.

But with the workout wear giant reporting first quarter earnings tonight, is there potential for a turnaround?

Q4 Fireworks and Q1 Comforts

On its fourth quarter release in March, shares of Lululemon were tripped up with a 15.8% spill.

This, despite the fact the company topped analysts’ expectations.

This issue – as is usual - was first quarter guidance… It forecast revenue of $2.19 billion (below the $2.25 billion Wall Street was looking for) with earnings of $2.37 per share (below the consensus of $2.55 per share).

The red flags were flying as this guidance marked a dramatic slowdown in growth. Let me explain… In the fourth quarter, Lululemon’s sales grew 16%, led by international sales growing 54%. But that first quarter guidance is projecting growth of just 9%.

So, that’s the waistband snap that stung investors.

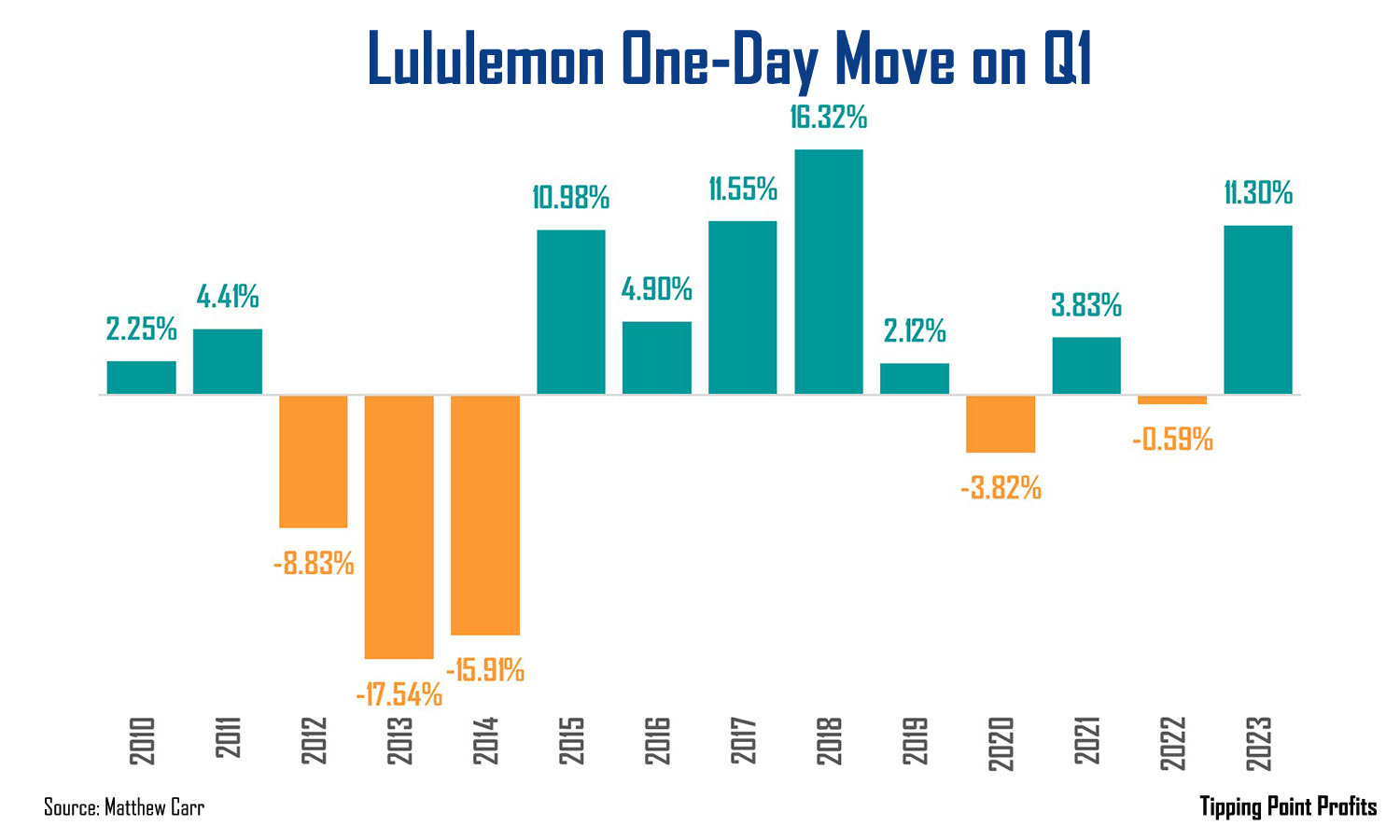

Now, I will say this… Historically, the reaction to fourth quarter results tends to be a wild one for Lululemon. Shares have seen moves of 9% or more (gains and losses) seven times in the last nine years.

For a tech company, that would be a wild ride. For an apparel company, that’s mayhem.

Well, the bright side is the trend has been a lot more positive for first quarter earnings reactions. In fact, shares have risen on this report seven of the past nine years…

And we can see four of those seven gains have been for 10% or more.

At the moment, the retail space is still grappling with an uncertain demand scenario… particularly in the U.S.

But I will add, the last time we saw shares of Lululemon get trounced on fourth quarter results as much as they did in March, was fourth quarter 2016. Shares collapsed 23.4% as first quarter 2017 guidance was for a single-digit loss in sales. The company would go on to report a 5% increase in revenue for the first quarter. And as we see in the chart above, shares leaped 11.5% on the results.

The options market is currently forecasting a +/-10.6% move on Lululemon shares tonight. Based on yesterday’s close of $306.78, that would take us as high as $339.16, or as low as $274.41.

The VertEA average one-day gain on Lululemon shares on first quarter earnings since 2010 is 1.5%. But since 2015, it’s been a gain of 6.29%.

The trend has been particularly optimistic for this global* athletics wear company on first quarter earnings. Historically, this is when Lululemon’s falling knife clatters to the ground. And I’d be hesitant to bet against it.

Not lounging today,

Matthew

"A falling knife has no handle ... and spills blood" ... right, Matt?

Going Taoist on us, Matt? (Kidding ... your opening is powerfully expressive/nicely executed ... I can "see" it ... and instantly understand where you're going). Nicely done.