We’re in the heart of big tech earnings.

As expected, Microsoft (MSFT) shares are pushing higher on a beat. But it’s not enough to offset the double-barrel 9% declines from Alphabet (GOOGL) and Alphabet (GOOG).

Well, tonight, there’s another key name set to report… Meta Platforms (META).

This is a name I’ve scored tremendous wins on over the years, both to the up- and downside.

In fact, exactly almost a year ago, on the morning of October 26, 2022, I wrote this note to my subscribers:

“Meta is pouring billions into the Metaverse, which is failing. The actual number of Metaverse users is shockingly low… and is basically just a bunch of dudes…”

I outlined on top of that, ad spend was drying up, like what we were seeing with other social media platforms, such as Snap (SNAP). And that Meta was the most exposed to the privacy policy changes that Apple (APPL) instituted that were dragging on tech results across the board in 2022.

To capitalize on Meta’s tailspin, we bought the November 4, $125 puts.

Less than 24 hours later, we rang the register with a 400% gain. For several of my new subscribers, the losses of 2022’s bear market were erased with a single play.

But remember, I focus on trends. So, my tune shifted as Meta transitioned away from the dumpster fire that is the Metaverse.

In fact, on April 25, 2023, I explained to Money Morning LIVE viewers why they should expect at least a 5.4% jump on Meta shares on first quarter earnings. And that a move closer to 17% was in store. Shares surged 13.9%... and went on to rally to new 52-week highs.

Then, on the social media’s second quarter results in July, I wrote that a move similar to what we saw in 2020 – where shares jumped 8.2% - could be in the cards. They ended the day up 4.4% after rocketing 8.9% higher.

Well, after the closing bell today, Meta will report third quarter results. Expectations are for $31.65 billion in revenue with earnings of $3.42 per share. That’s more than a 100% increase in earnings from a year ago.

So, is this the moment to go all-in?

To bet on a jump higher in Meta’s shares (as I said to expect from Microsoft)?

Or is this a redux from 2022?

Well, let’s explore what VertEA has to say…

60% Chance for a Drop

First, it’s worth noting that Meta is facing lawsuits from 33 state attorney generals for its role in the mental health crisis among teens in the U.S. This is on top of the 8 attorney generals that have sued the company in state courts on similar charges, with Florida suing Meta in a federal lawsuit.

Second, Meta is benefiting from the exodus from X/Twitter. When the company launched Threads in July – its Twitter competitor - it took a mere five days to accumulate 100 million users. That smashed all previous records for app adoption, including the two months it took for ChatGPT to reach that milestone.

But it admittedly has been touch-and-go to keep those users engaged and on platform. For instance, in September, Threads averaged a mere 10.3 million daily active users (DAUs). That’s a decline of 79% from its peak and a fifth of X’s current daily audience. Though, Meta expects to grow DAUs to nearly 24 million by year’s end.

So, there are still significant hurdles for Meta ahead.

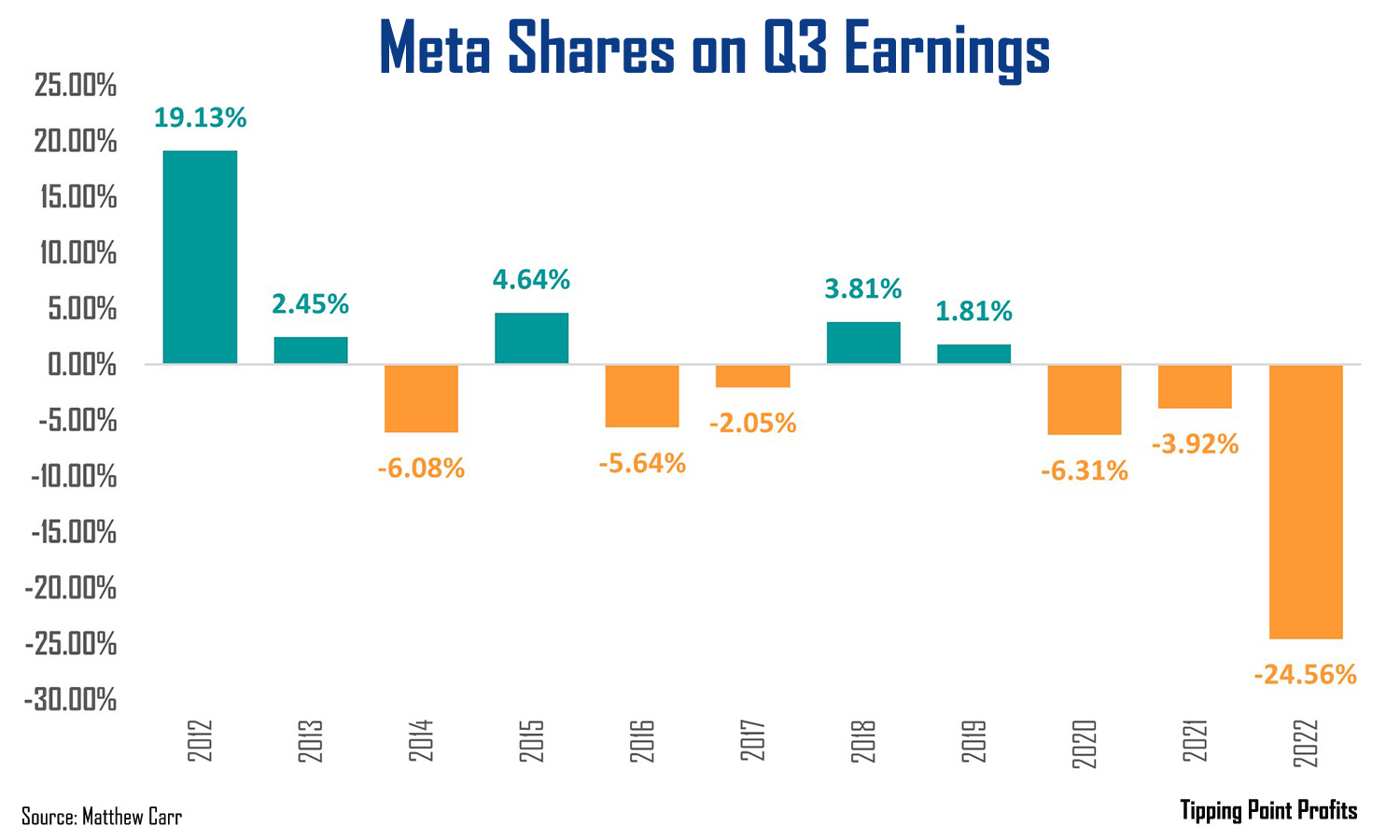

On top of that, history tells us to temper our expectations on third quarter earnings…

Meta shares have fallen on this report six of the last 10 years. And that includes three consecutive years of declines, as well as last year’s massive 24.6% plunge. Since going public, the social media giant has averaged a one-day loss of 1.52% on this report, making it by far its worst-received report of the year.

It’s also important to note the moves on this report tend to be outsized. In fact, over the last 11 years, Meta shares have seen 8 one-day moves greater than 3.75%.

Now, a drop doesn’t mean the company is in trouble or facing dire headwinds. It just means that Meta – like Microsoft – has a cyclical nature to its business. And the third quarter is typically one of its softest stretches of the year.

But as we look down the road to the fourth quarter, Meta’s business really starts to take off. Remember, at its core, it’s merely a glorified advertising company. And with the holiday season in full swing, expectations are for fourth quarter revenue of $36.64 billion with earnings of $4.56 per share. So, we can see that’s a step up from what we’re looking for this evening from Meta’s third quarter earnings.

September and October are the worst months of the year for Meta shares. They just eked out a gain of 0.28% in September – their first gain in the month since 2016. And they’re currently up a little more than 0.50% in October – a month they’ve ended lower four out of the last five years… all due to investor reaction to third quarter earnings.

Something to keep in mind this evening.

Not banking on a Thread-fueled rally,

Matthew

P.S. My friends at the MoneyShow organization have assembled a dynamite lineup of world-class market strategists, economists, professional traders, money managers, and newsletter publishers.

You’ll have the opportunity to hear and learn from the likes of...

Charles Payne, Host, Fox's Making Money with Charles Payne

George Gilder, Editor, Gilder's Technology Report

Lindsey Piegza, Chief Economist, Stifel Financial Corp.

Barry Ritholtz, Founder and CIO, Ritholtz Wealth Management

Mark Skousen, Editor, Forecasts & Strategies

John Carter, Author, Mastering the Trade

Howard Tullman, General Managing Partner, G2T3V, LLC

And more than 75+ other experts! They’ll cover everything from stocks, bonds, real estate, energy, and precious metals to alternative investments and elite trading tools and strategies. Plus, the conference is being held at the Omni Orlando Resort at ChampionsGate – one of the nation's premier golf, meeting, and leisure retreats.

The event runs from October 29 to October 31. And since you are valued readers, MoneysShow has prepared a special offer. Merely click here to take advantage of a “flash pass” to see myself and dozens of other industry experts.

Before you go rushing off to do all those things that make you great, do me a favor … Don’t worry, I’m not asking for money. But if you like what you read here, give me a like, comment or share this article with a friend. If you didn’t enjoy what you’ve read, tell me why. I’m not promising you won’t hurt my feelings, but I’m open to suggestions for improving content!

© 2023 Matthew Carr

All rights reserved.

Any reproduction, copying, distribution, in whole or in part, is prohibited without permission.

This market commentary is opinion and for entertainment purposes only. The views and insights shared by the author are based on his many years of experience covering the markets. But they are subject to change without notice and opinions may become outdated. And there is no obligation by the author to update any information if these opinions become outdated. The information provided is obtained from sources believed to be reliable. But the author cannot guarantee its accuracy. Nothing in this email should be considered personalized investment advice. Investments should be made after consulting your financial advisor and after reviewing the financial statements of the company or companies in question.

Thank you Matthew for your analysis. Same as Gerald, I also miss your recommendations at Oxford.

You’ve mentioned the VertEA strategy a number of times. Is there a good source to either obtain the completed information or the pieces?